portability estate tax exemption

2022-32 qualifying estates may file an estate tax return to request portability of the decedents unused estate tax exemption up to the fifth anniversary of the decedents date of death. The first 25000 of this exemption applies to all taxing authorities.

Tax Portability Transfering Your Tax Benefits From Your Old Homestead To Your New One

Therefore the objective should be to get the survivors estate at or below the 4000000 threshold for Illinois.

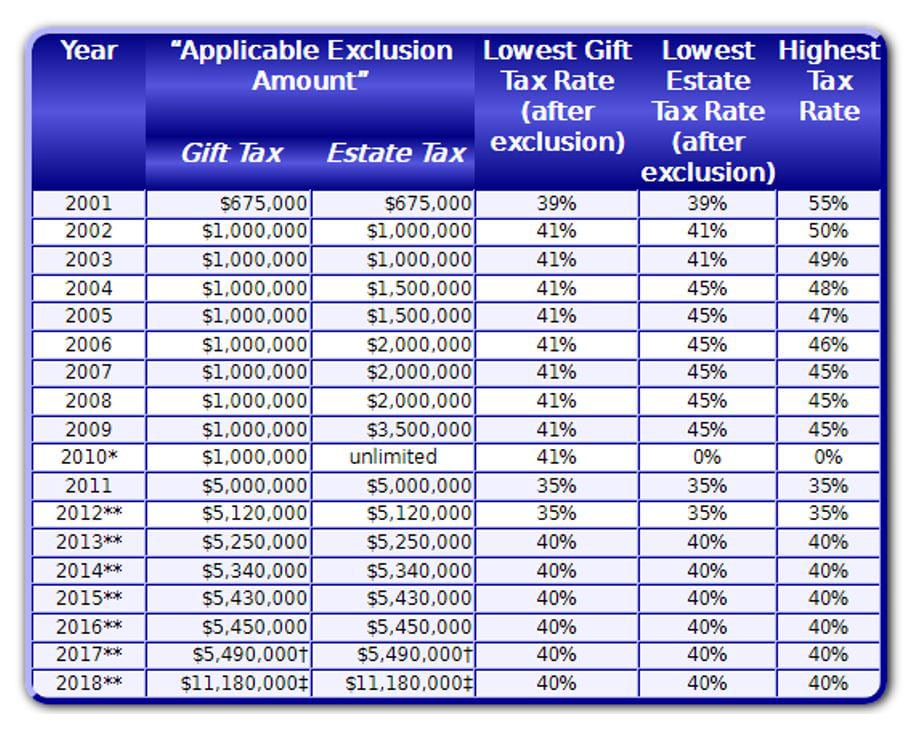

. Portability of the estate tax exemption means that if one spouse dies and does not make full use of his or her 5000000 in 2011 or 5120000 in 2012 5250000 in 2013 5340000 in 2014 and 5430000 in 2015 federal estate tax exemption then the surviving spouse can make an election to pick up the unused exemption and add it to the. Please note these laws being permanent means that they are not set. As of that time the estate tax exemption was much lower.

When the surviving spouse later dies or makes a lifetime gift the surviving spouse will have his or her own. This post will discuss the general rules of portability. The concept of portability does.

If the portability election is filed in time the entire estate of 60 million will be named under the wife. And then after one spouses death then the surviving spouse can take steps to combine their estate tax exemptions to reduce estate tax. Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706.

State law allows Florida homeowners to claim up to a 50000 Homestead Exemption on their primary residence. With inflation this may land somewhere around 6 million. Portability allows any unused portion of the estate tax exemption to be transferred to the surviving spouse.

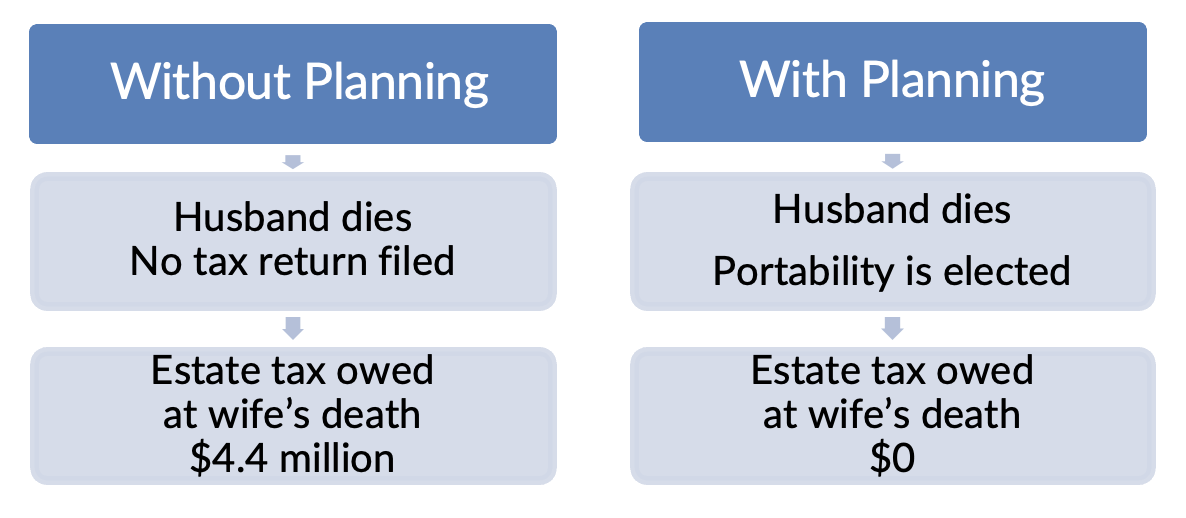

Without portability if the first spouse died with an estate of 3000000 all of which passed to the Trust Exempt from Estate the deceased spouses unused estate tax exemption of 8400000 would be lost. A married couple can pass up to 10960000 free of Federal estate tax. The wife has to file the IRS Form 706 federal estate tax returns to get the portability within 270 days after her husbands death.

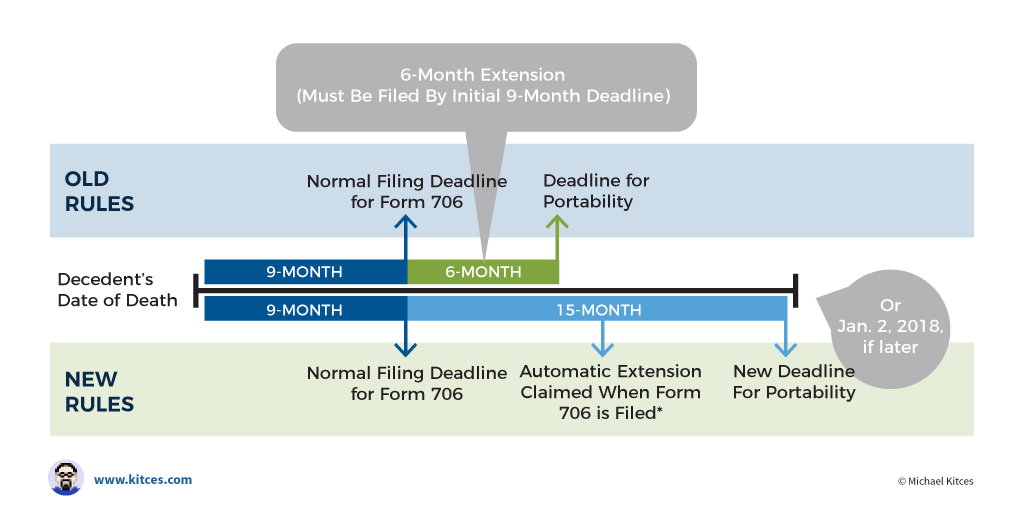

2010 c 5 A if that estate was not required by Sec. In order to benefit from this exemption however the surviving spouse must file IRS Form 706 the United States Estate and Generation-Skipping Transfer tax return within nine months of the first death in order to elect portability. Under the current tax law the higher estate and gift tax exemption will Sunset on December 31 2025.

This was just the estate tax portability rules though. 6018 a to file an estate tax return. 2017-34 this simplified method which is used in lieu of the letter.

3019100-3 to make a portability election under Sec. If during hisher lifetime the survivor. Absent further legislation in 2013 the exemption amount will be reduced to 1000000 and the top tax rate will once again be 55.

The Tax Cuts and Jobs Act increased the federal estate tax exemption in 2018 and it has increased since then adjusting with inflation so its no surprise that the exemption is higher for 2022. Estate planning remains important as the provisions of the Congressional bill informally known as the Tax Cuts and Jobs Act approved by the House and the Senate and sent to the President for signature on December 20 2017 the Tax Bill offer. Each taxpayer has a fixed amount of asset value that can escape estate tax at the time of death an exemption.

As the year draws to a close much is expected to change with respect to income estate and gift taxes as a result of tax reform. 2017-34 the IRS provided a simplified method for obtaining an extension of time under Regs. The key advantage of portability is flexibility.

Starting January 1 2026 the exemption will return to 549 million adjusted for inflation. After 2012 one important question for estate planning is whether or not portability should be elected at the first death. 6018a as determined based on the value of the gross estate and adjusted taxable gifts Reg.

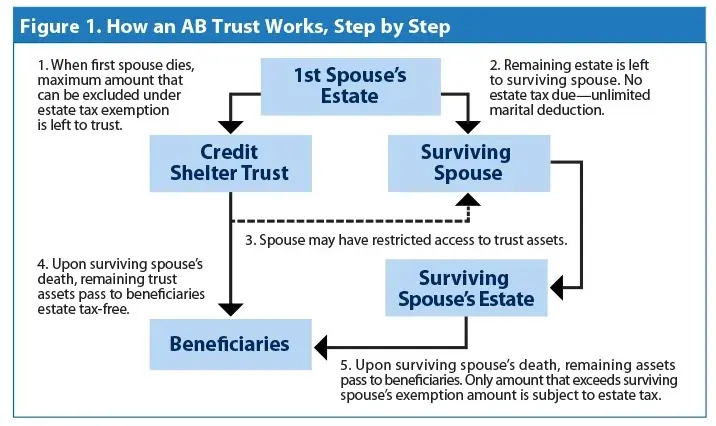

The need for splitting the estate into. The non-exempted amount of 545 million would be portable and would be passed to his wife. The Illinois estate tax on an estate of 16880000 would be 1524400.

The 5000000 exemption amount will be indexed for inflation in 2012. After all electing portability could mean that a surviving spouse could have double the estate tax exemption at the second death currently 5430000 x 2 10860000. The second 25000 excludes School Board taxes and applies to properties with assessed values between 50000 and 75000.

A portability election allows a surviving spouse to use leftover exemption amounts from the first-to-die spouse so there is a chance that the surviving spouses personal exemption can be combined with the leftover exemption from the first-to-die spouse to shield the surviving spouses estate from the estate tax too. The federal estate tax exemption is indexed for inflation so it increases periodically usually yearly. Using the current 5 million exemption amount a surviving spouse could potentially end up with a 10 million exemption.

For decedents dying in 2011 and 2012 the personal representative can elect to transfer the deceased spouses unused exemption to his or her surviving spouse. If the surviving spouse died with assets exceeding the federal estate tax exemption the surviving spouse could not use the lost exemption. 202010-2a1 clarifies that the due date of an estate tax return required to elect portability is nine months after the decedents date of death or the last day.

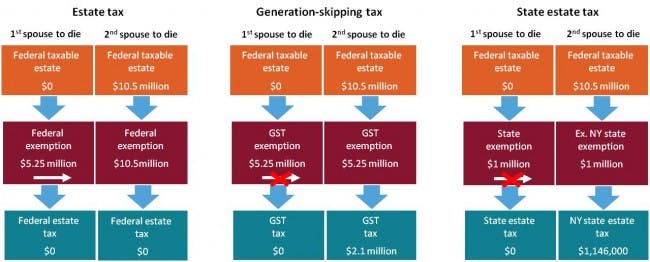

Under the Act the federal estate tax exemption is set at 5000000 and the top estate tax rate is 35. Portability between spouses means that any unused Federal estate exemption of the first spouse to die can be added to the surviving spouses exemption for the. Portability also applies to gift tax and therefore the gift tax exemption is also 16880000 for the survivor.

It allows the spouses to go about their estate planning and transfer assets upon their death the way that they would like to to carry out their wishes. Historically Portability could only be accomplished through the use of proper trust based planning. Federal Estate GST and Gift Taxes For 2016 the Federal estate tax exemption rises 90000 to 5480000.

What happens to the federal estate tax exemption in 2026. For estates that are not required to file an estate tax return under Code Sec.

Is Ab Trust Planning Still Effective

Portability Becomes Permanent Baker Tilly

Gkmvdiykqh3sfm

Tax Related Estate Planning Lee Kiefer Park

Locking In A Deceased Spouse S Unused Federal Estate Tax Exemption

Exploring The Estate Tax Part 2 Journal Of Accountancy

What Surviving Spouses Need To Know About The Marital Portability Election Natural Bridges Financial Advisors

Estate Planning Can Secure Your Legacy Jackson Fox Pc Ardmore Ok

Understanding Qualified Domestic Trusts And Portability

Credit Shelter Trusts And Portability Eagle Claw Capital Management

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel

Portability Of A Spouse S Unused Exemption 1919ic

Portability Of A Spouse S Unused Exemption 1919ic

Portability Enabled Traditional Trusts Clark Trevithick Full Service Boutique Law Firm In Los Angeles California Southern California

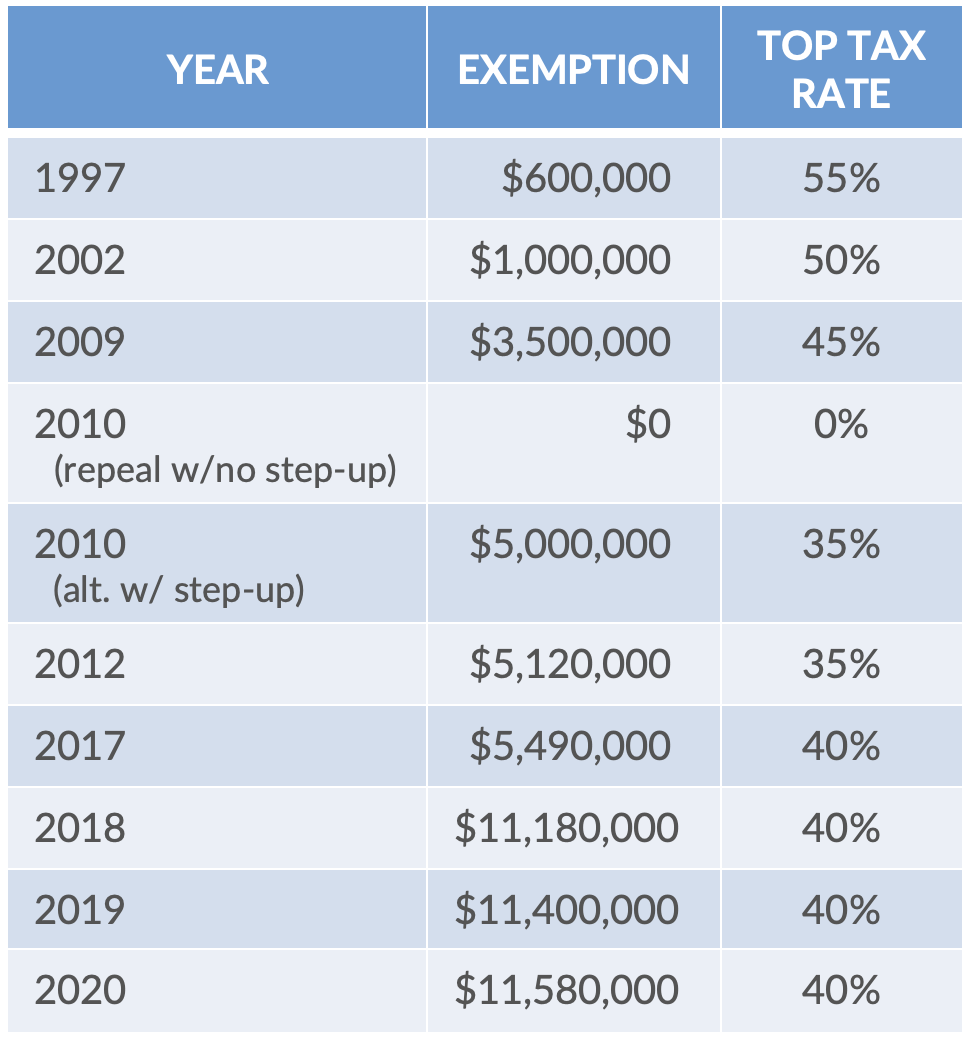

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Portability Of Unused Estate And Gift Tax Exclusion Between Spouses

Form 706 Extension For Portability Under Rev Proc 2017 34

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Untitled Document